Tax pooling is one of those tools most business owners wish they knew about earlier. If you’ve ever missed a provisional tax payment and got slapped with IRD interest or penalties, this could be your lifesaver.

Instead of paying IRD directly, you buy tax that someone else already paid on time. IRD sees it as if you paid on time too. That means no late penalties, lower interest, and more flexibility with how and when you pay.

If your cash flow’s tight or you’ve underpaid, tax pooling gives you room to breathe. In this article, we’ll show you how it works, when to use it, and how providers like TMNZ and Tax Traders can help you take control of your tax bill.

What is tax pooling in New Zealand?

Tax pooling is an IRD-approved system that lets businesses pay their income tax late without getting hit by late payment penalties or high interest.

Instead of paying IRD directly your Terminal Tax or Provisional Tax, you work with a tax pooling provider like TMNZ or Tax Traders. These providers hold tax payments from other businesses in a “pool.” You then purchase the tax you need from that pool, and IRD treats it as if you paid on time.

This is especially useful if:

- You missed a provisional tax deadline

- You underpaid and owe terminal tax

- You want to avoid IRD’s use-of-money interest (UOMI)

How does tax pooling work?

Here’s a simplified breakdown of how tax pooling actually plays out:

Step-by-step:

- You realise you missed a provisional tax payment or owe more than expected

- You contact a tax pooling provider

- You purchase tax that another business paid earlier

- The provider transfers the tax to IRD on your behalf, backdated to the original due date

IRD then applies that payment to your account as if you paid on time, wiping out late payment interest and penalties.

When should you use tax pooling?

Tax pooling isn’t just for emergencies. It’s a smart tool for planning, smoothing out cash flow, and staying flexible.

You might use it when:

- You underpaid your provisional tax

- You received a reassessment from IRD

- You didn’t know what your income would be (start-up, seasonal work, big contracts)

- You want to pay tax in instalments, not lump sums

- You want to reduce IRD’s interest costs

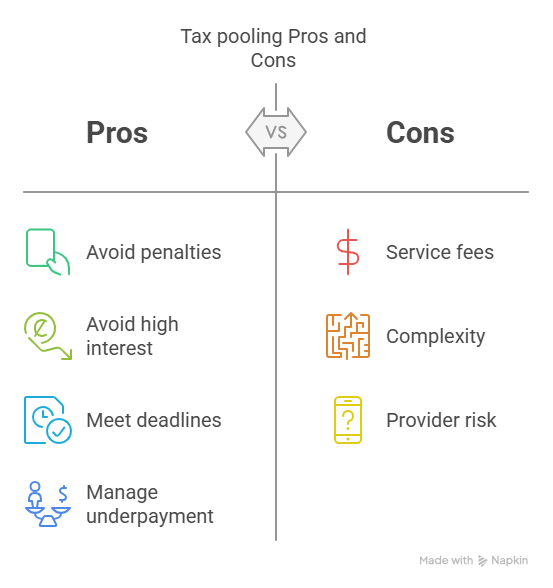

Tax pooling vs paying IRD directly

Still not sure if it’s worth it? Here’s a side-by-side look at the key differences:

Table – Tax pooling vs IRD direct payment

| Feature | Tax Pooling | IRD Direct |

|---|---|---|

| Missed deadline? | ✅ Still accepted | ❌ Penalties apply |

| Interest charged? | ✅ Yes (but lower) | ✅ Yes (UOMI applies) |

| Payment flexibility? | ✅ Pay in instalments | ❌ Must pay in full |

| IRD approved? | ✅ Yes | ✅ Yes |

| Can backdate payment? | ✅ Yes | ❌ No |

Real example: Tax pooling in action

Let’s say you were meant to pay $20,000 provisional tax on 28 August, but didn’t. IRD starts charging interest straight away and penalties follow soon after.

In October, you realise the error and contact Tax Traders. They find another business that paid $20,000 into the tax pool on 28 August. You buy that tax from them.

Tax Traders then transfer that $20,000 to IRD on your behalf, dated 28 August. IRD wipes the interest, applies it to your account, and you’re all good.

Who offers tax pooling in NZ?

There are two main IRD-approved tax pooling providers:

- TMNZ (Tax Management NZ)

- Tax Traders

Both offer easy online systems, flexible payment plans, and can work directly with your accountant.

Tip:

You can’t set up tax pooling through IRD. It must be done through one of these providers, ideally with guidance from your tax agent. If you’re not sure how provisional tax works in the first place, check out our upcoming article on provisional tax threshold & dates.

Conclusion: Tax pooling buys you time (and peace of mind)

Tax pooling isn’t a loophole or a last resort. It’s a smart, IRD-approved way to take control of your provisional tax without getting smashed by penalties and high interest.

If you’ve missed a payment, underestimated your income, or just want more flexibility, tax pooling lets you backdate your payment, spread the cost, and stay compliant — all without upsetting your cash flow.

Whether you work with TMNZ, Tax Traders, or through your accountant, it’s one of the best-kept tax secrets in the game.

And if you’re not sure whether it’s right for you, BH Accounting is here to walk you through it.

FAQ about tax pooling in NZ

Is tax pooling legal?

Yes. It’s IRD-approved and has been used in New Zealand since 2003.

Can individuals use tax pooling?

Yes, if you have large tax bills — but it’s mostly used by businesses and trusts.

How long do I have to use tax pooling?

You have up to 75 days after your terminal tax date to use it.

Can I use tax pooling for past tax years?

Yes — within time limits. It can apply to current or prior years, depending on your situation.

Does tax pooling change my tax return?

No. It just affects how and when the payment is made to IRD — not your reported income.

Disclaimer

This article is for information only—not legal, financial, or tax advice. Every business is different, and rules change, so don’t make major decisions based on what you read here. If you’re unsure, talk to a professional—it’s cheaper than fixing a costly mistake later.